Make no mistake, Iran’s return to the oil market is going to have a significant impact on the Oil & Gas industry for the later part of 2015 and as we head into 2016.The headline is this: prices are low and they’re going to stay low. For industry leaders, many of who have already begun implementing measures to drive inefficiencies out of their businesses, watching and waiting is simply not an option. The message to them is this; it’s not too late to shore up your strategic future, but you need to act now. There’s no doubt that oversupply and lower prices represent a real challenge to the industry, but that doesn’t mean the future is all gloom. It just means that producers and refiners need to adopt strategies to prepare for the new reality.

Why low prices are here to stay

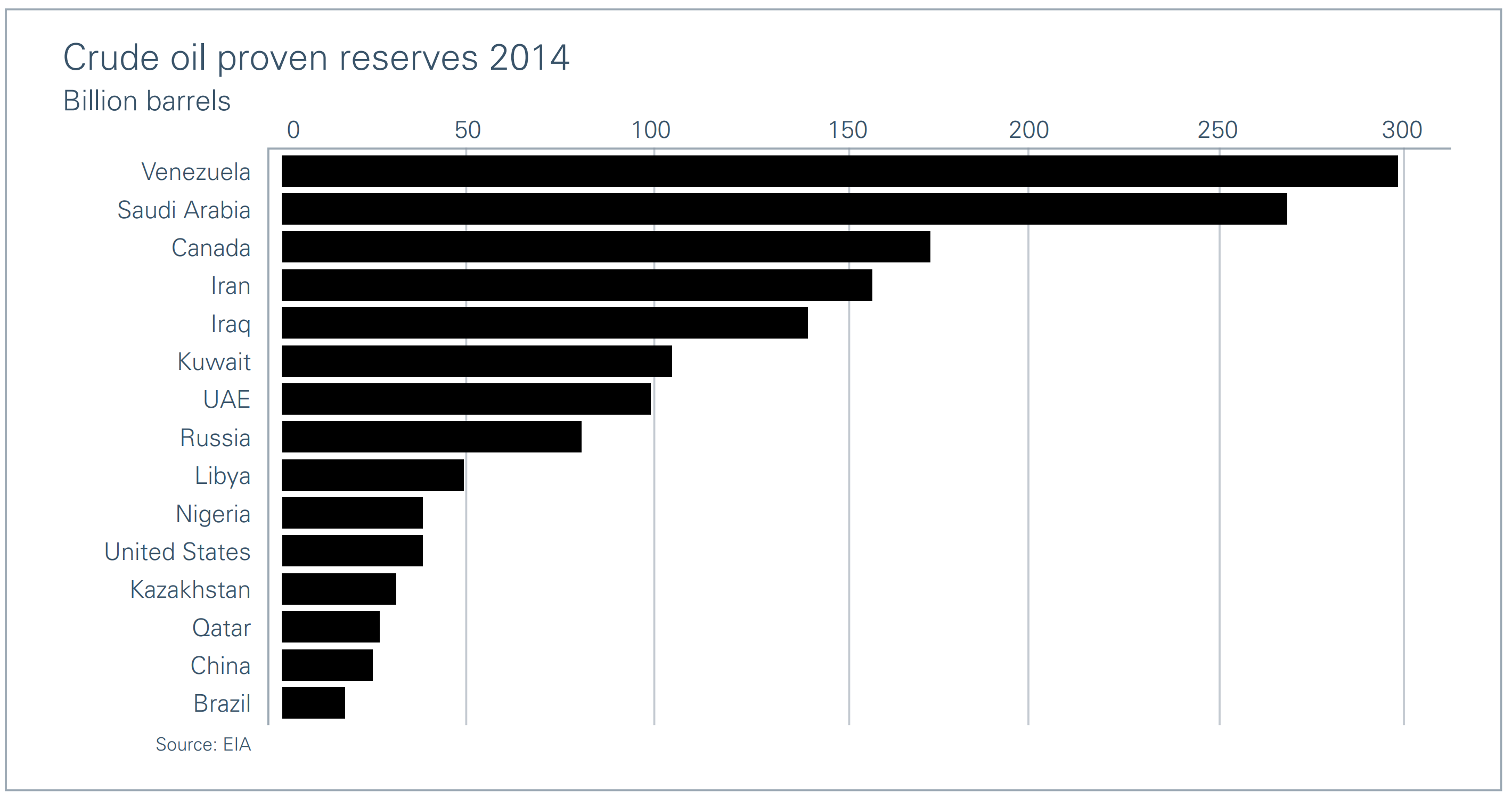

Iran was once OPEC’s largest oil producer and has the world’s fourth largest proven crude oil and the second biggest natural gas reserves. As a result of the nuclear deal with the west, new flows of Iranian fuel could hit an already over-supplied market in a matter of months. A Reuters poll of 25 oil analysts from leading banks and brokerages forecast that Iran would be able to raise oil output by between 250,000 and 500,000 bpd by the end of 2015. Added to this, US crude oil output in 2015 is, according to US Energy Information

Administration, “on track to be the highest in 45 years,” and, according to Platts, OPEC is now producing 31.5 million bpd- that’s the most since 2012.1

All of this means that, for the foreseeable future, over-production will continue to cause a significant global supply glut, and that in turn means prices will stay low. So, how do you survive and thrive in a market that is oversupplied? The answer is simple; the only way to drive up profits is to drive down costs and that means looking deep into your value chain to identify where savings can be made.

“Iran’s return is set to keep oil prices lower for longer alongside evercheaper shale oil and peaking world demand, said Norbert Ruecker, head of commodities research at Julius Baer.

Fundamental differences between the 2015 downturn and the one that occurred in 2008

The primary difference is that the downturn in 2008 was comparatively short lived. Some belt tightening took place but many companies went back to old habits once the price went up. This meant they didn’t address some of the fundamental operational efficiencies in their businesses. Towards the end of 2014, the level of water in the pond dropped significantly, exposing these operational inefficiencies once again and, this time, those companies who ignore them do so at their peril.

It’s fair to say that the majority of organizations in the value chain were anticipating recovery to be slower than in 2008 but the Iranian agreement makes this an absolute certainty. This has created a real imperative for companies to drive operational inefficiencies out of their businesses if they want to remain competitive.

Impact on the North American Gas & Oil Industry

The greatest impact so far has been felt in the upstream area where more restriction has occurred. However the changes are also impacting the midstream. The challenge in the midstream market has to deal with extra capacity in storage. To do this, companies need to increase velocity across their assets to move product without introducing more capital to the business. The downstream sector is focused on optimizing their facilities to take advantage of low commodity prices and over supply, which is resulting in record profits.

What we are seeing this year and into 2016 will strengthen North America’s position as a global swing producer. There are a few key reasons why the US has been so proficient and prolific. The first is that the position is based on 4,000 entrepreneurial producers ratcheting up. The second is the release of individual land rights, this broader benefit has helped fuel our swing producer status. The final point is that there has been a vast amount of access to capital investment. The US has been able to flex drilling investment and capacity, which has meant North American producers have been able to maintain aspects of competitiveness.

“Many of the senior executives we have met are already looking at areas that they have traditionally missed from an operational or process perspective, looking deeper into their value chain to reduce their direct spend.”

Having said that, the future is far from certain given the high level of production from the OPEC nations and now from Iran. The industry has already demonstrated a surprising capacity to be innovative and lower costs where necessary. Many of the senior executives we have met are already looking at areas that they have traditionally missed from an operational or process perspective, looking deeper into their value chain to reduce their direct spend. Many of them have already taken the low-hanging fruit out and need to take a deeper value optimization view across their business.

Overcoming organizational hurdles: doing ‘more with less talent’

From an organizational standpoint, the first challenge is around people. Doing what was OK in the past is not sufficient. This means looking at new ways of optimizing your people and teams, and that can be a major challenge. Often executives are expected to do ‘more with less’ given significant layoffs. Overcoming this challenge and changing the mindset of their people is key.

The other hurdle they face is the exit of the baby boomers. Especially in the smaller firms, there are often only a small number of people who have the long-term experience needed to address some of these issues. Many employees who have been in the industry in the past 5-7 years have not dealt with typical issues being faced today – leaving a vacuum of talent and industry insight. As a result firms have to increasingly look outside the four walls of their organization to help infuse talent and capability and help them optimize their operations to deliver sustainable performance improvement.

Four operational improvement areas many oil companies have overlooked

Lower oil prices are the new reality so now the fundamental challenge for executives is to identify further areas for operational improvement to protect and enhance their profit margin.

In our experience, companies frequently overlook the potential for savings in 4 key areas:

1. Get more out of suppliers and service providers

The drop in oil prices makes this opportunity even more compelling. We often meet executives and CPOs who are confident that their procurement process is mature only to discover that they are leaving millions of dollars on the table. Finding out where your procurement team is on the maturity curve and understanding the potential benefits for improvement is a powerful way to quickly improve your cost and competitive base. For example, we assisted a large North American oil company to capture over 27% in procurement savings.

2. Major savings can be made in your Crude and Refined Product logistics operation

Crude and refined product transportation is another area that is frequently overlooked. Many executives simply aren’t aware that they can overcome the challenges posed by congested modes and networks by achieving stronger, more strategic relationships with carriers simultaneously reducing costs and improving performance. We helped a major joint venture between Mid-Stream companies to increase its takeaway capacity by 43% and improve fleet asset utilization by 31%.

3. More efficient capital projects and plant turnarounds

Focus on fast and efficient turnarounds without compromising safety. Cost savings initiatives are obviously critical in times like these, however just as important is ensuring scheduled plant turnarounds run on time, under budget and with a 100% safety record. For example, one of the world’s largest oil companies called us in when they were just 3 months away from a scheduled shutdown. With our help, the executives prepared for and conducted the largest turnaround in their plant’s history with zero accidents or spills, saving millions per day.

4. Remote Site & Offshore Services / Field Logistics offer significant untapped cost

savings potential

If you’re already spending tens, if not hundreds, of millions of dollars a year on remote site services such as aviation, ground transportation and lodgings, you may well be missing out on opportunities to decrease wasted resources, reduce your carbon footprint and tap into unrealized savings in the millions of dollars. We identified 35% in savings on optimization alone for the lodging division of a major integrated energy company. Continued negotiations with service contractors are expected to yield millions of dollars in additional savings. In addition we achieved savings of 22% for their aviation division and reduced their ground transportation costs by 7% in just 7 months.